Announcements & Reminders

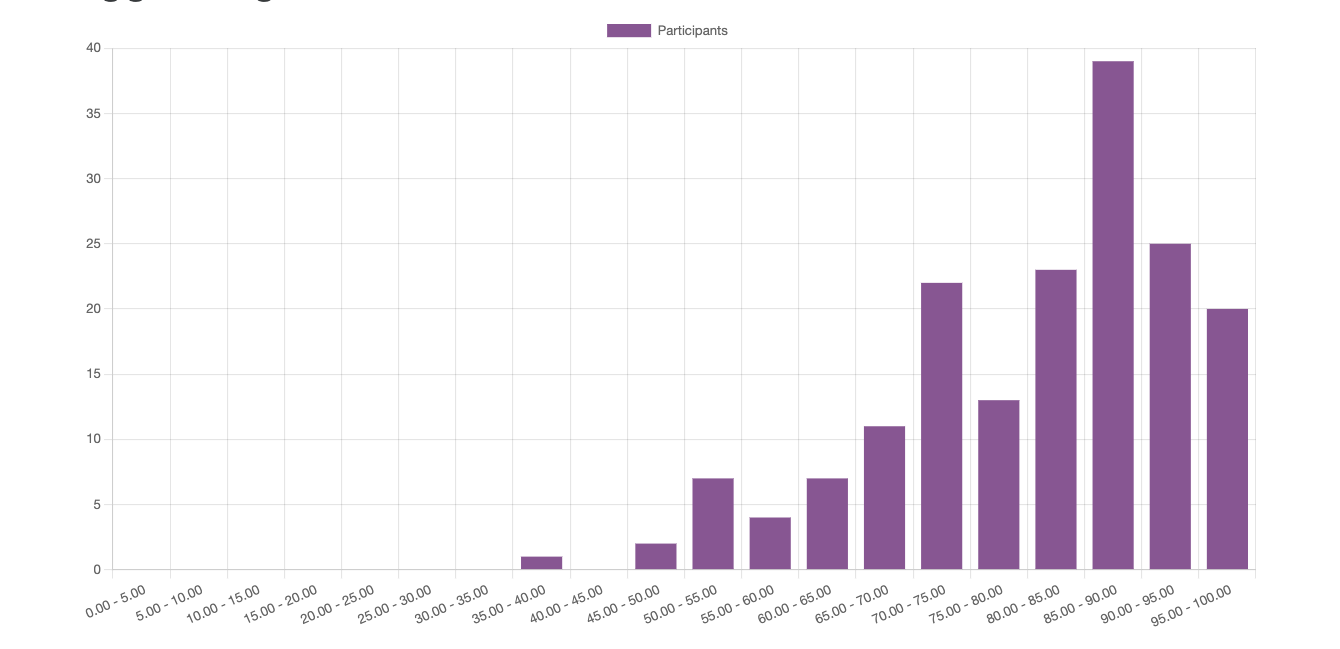

Quiz 2

Fig. 51 Distribution of results for Quiz 2#

The midterm is scheduled at 18:30 to 19:45 (1 hour + 15 min reading time) on Monday, April 15 in Melville Hall

Practice problems for the midterm to be published

SPECIAL NOTE

The material in this section of the lecture notes will be used in the quiz 3, however, the midterm and the final exams will not target detailed knowledge of this section. The exams will however require a practical knowledge of linear algebra needed for solving problems similar to the tutorial problems.

📖 Elements of linear algebra#

⏱ | words

Important note

This lecture covers the fundamental concepts of linear algebra, and covers more material than the time permits to cover in a single lecture

It is strongly advised to study the details of this lecture note is greater details in preparation for the midterm and final exams

I also encourage you to watch some or all of the videos in the 3Blue1Brown: Essence of linear algebra series at your own time to get deeper understanding of the linear algebra concepts through visualizations and excellent explanations

The lecture covers the following main concepts:

Vector space

Linear combination

Span

Linear independence

Basis and dimension

Matrices as linear transformations

Column spaces and null space

Rank of a matrix

Singular matrices

Matrix determinant

Eigenvectors and eigenvalues

Diagonalization of matrices

See references in the bottom of this note

Midterm and final exam may have some but not much of the material from this lecture because it is mainly left for self-study. Open book quiz, however, will contain questions for this material.

Motivating example#

Linear algebra is most useful in economics for solving systems of linear equations

Definition

A general system of linear equations can be written as

More often we write the system in matrix form

Let’s solve this system on a computer:

import numpy as np

from scipy.linalg import solve

A = [[0, 2, 4],

[1, 4, 8],

[0, 3, 7]]

b = (1, 2, 0)

A, b = np.asarray(A), np.asarray(b)

x=solve(A, b)

print(f'Solutions is x={x}')

Solutions is x=[-1.77635684e-15 3.50000000e+00 -1.50000000e+00]

This tells us that the solution is \(x = (0. , 3.5, -1.5)\)

That is,

The usual question: if computers can do it so easily — what do we need to study for?

But now let’s try this similar looking problem

Question: what changed?

import numpy as np

from scipy.linalg import solve

A = [[0, 2, 4],

[1, 4, 8],

[0, 3, 6]]

b = (1, 2, 0)

A, b = np.asarray(A), np.asarray(b)

x=solve(A, b)

print(f'Solutions is x={x}')

Solutions is x=[ 0.00000000e+00 -9.00719925e+15 4.50359963e+15]

/var/folders/5d/cjhpvdlx7lg8zt1ypw5fcyy40000gn/T/ipykernel_31662/3978225594.py:8: LinAlgWarning: Ill-conditioned matrix (rcond=4.11194e-18): result may not be accurate.

x=solve(A, b)

This is the output that we get:

LinAlgWarning: Ill-conditioned matrix

What does this mean?

How can we fix it?

We still need to understand the concepts after all!

Vector Space#

Definition

A field (of numbers) is a set \(\mathbb{F}\) of numbers with the property that if \(a,b \in \mathbb{F}\), then \(a+b\), \(a-b\), \(ab\) and \(a/b\) (provided that \(b \ne 0\)) are also in \(\mathbb{F}\).

Example

\(\mathbb{Q}\) and \(\mathbb{R}\) are fields, but \(\mathbb{N}\), \(\mathbb{Z}\) is not (why?)

Definition

A vector space over a field \(\mathbb{F}\) is a set \(V\) of objects called vectors, together with two operations:

vector addition that takes two vectors \(v,w \in V\) and produces a vector \(v+w \in V\), and

scalar multiplication that takes a scalar \(\alpha \in \mathbb{F}\) and a vector \(v \in V\) and produces a vector \(\alpha v \in V\),

which satisfy the following properties:

Associativity of vector addition: \((u+v)+w = u+ (v+w)\) for all \(u,v,w \in V\)

Existance of zero vector \({\bf 0}\) such that \(v + {\bf 0} = v\) for all \(v \in V\)

Existance of negatives: for each \(v \in V\) there exists a vector \(-v \in V\) such that \(v + (-v) = {\bf 0}\)

Associativity of multiplication: \(\alpha (\beta v) = (\alpha \beta) v\) for all \(\alpha, \beta \in \mathbb{F}\) and \(v \in V\)

Distributivity: \((\alpha + \beta) v = \alpha v + \beta v\) and \(\alpha(v+w) = \alpha v + \alpha w\) for all \(\alpha, \beta \in \mathbb{F}\) and \(v, w \in V\)

Unitarity: \(1u = u\) for all \(u \in V\)

may seem like a bunch of abstract nonsense, but it’s actually describes something intuitive

what we already know about operations with vectors in \(\mathbb{R}^N\) put in formal definition

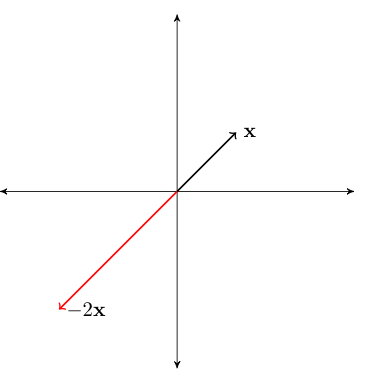

Example

Example

Fig. 52 Scalar multiplication by a negative number#

Dot product and norm#

Definition

The dot product of two vectors \(x, y \in \mathbb{R}^N\) is

The notation \(\square^T\) flips the vector from column-vector to row-vector, this will make sense when we talk later about matrices for which vectors are special case.

Fact: Properties of dot product

For any \(\alpha, \beta \in \mathbb{R}\) and any \(x, y \in \mathbb{R}^N\), the following statements are true:

\(x^T y = y^T x\)

\((\alpha x)' (\beta y) = \alpha \beta (x^T y)\)

\(x^T (y + z) = x^T y + x^T z\)

Definition

The (Euclidean) norm of \(x \in \mathbb{R}^N\) is defined as

\(\| x \|\) represents the ``length’’ of \(x\)

\(\| x - y \|\) represents distance between \(x\) and \(y\)

Fact

For any \(\alpha \in \mathbb{R}\) and any \(x, y \in \mathbb{R}^N\), the following statements are true:

\(\| x \| \geq 0\) and \(\| x \| = 0\) if and only if \(x = 0\)

\(\| \alpha x \| = |\alpha| \| x \|\)

\(\| x + y \| \leq \| x \| + \| y \|\) (triangle inequality)

\(| x^T y | \leq \| x \| \| y \|\) (Cauchy-Schwarz inequality)

Linear combinations#

Definition

A linear combination of vectors \(x_1,\ldots, x_K\) in \(\mathbb{R}^N\) is a vector

where \(\alpha_1,\ldots, \alpha_K\) are scalars

Example

Fact

Inner products of linear combinations satisfy

Proof

Follows from the properties of the dot product after some simple algebra

Span#

Let \(X \subset \mathbb{R}^N\) be any nonempty set (of points in \(\mathbb{R}^N\), i.e. vectors)

Definition

Set of all possible linear combinations of elements of \(X\) is called the span of \(X\), denoted by \(\mathrm{span}(X)\)

For finite \(X = \{x_1,\ldots, x_K\}\) the span can be expressed as

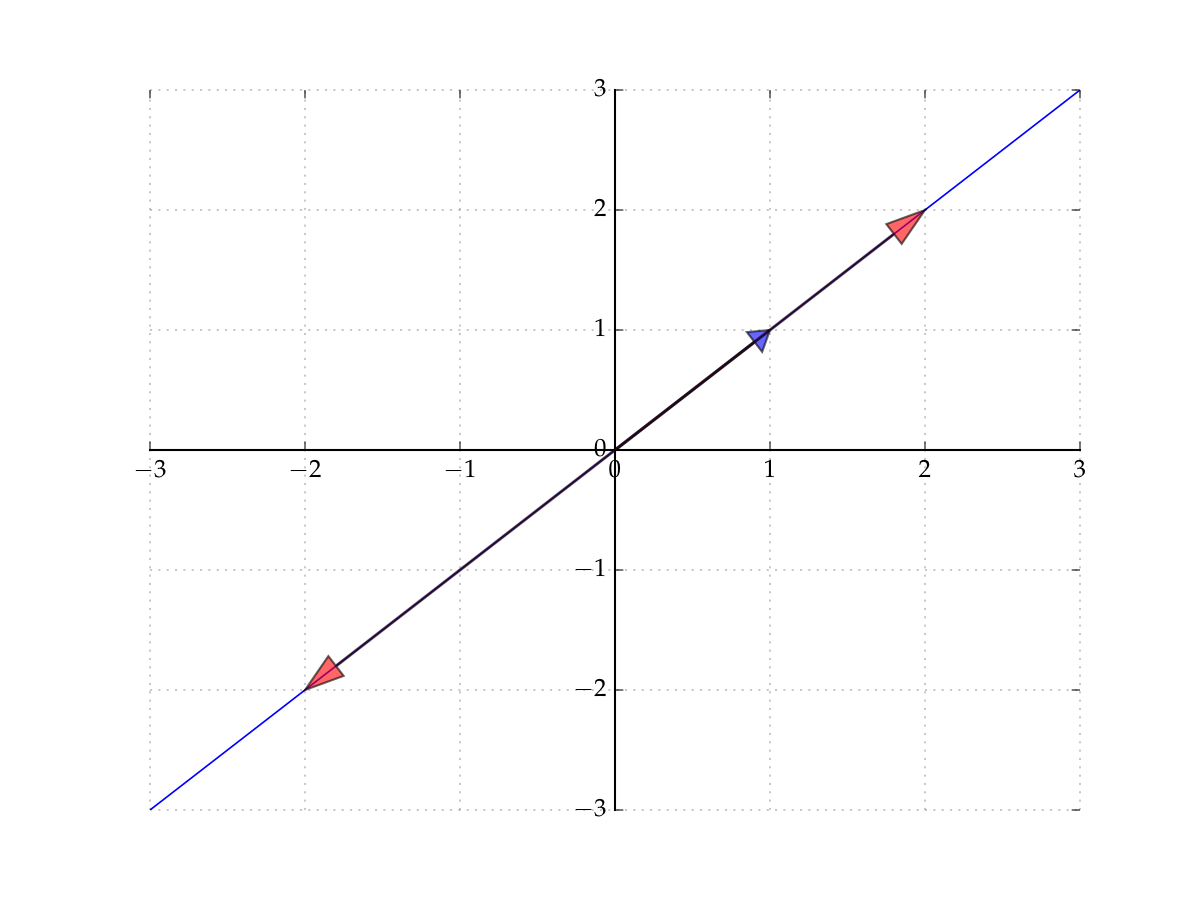

Example

Let’s start with the span of a singleton

Let \(X = \{ (1,1) \} \subset \mathbb{R}^2\)

The span of \(X\) is all vectors of the form

Constitutes a line in the plane that passes through

the vector \((1,1)\) (set \(\alpha = 1\))

the origin \((0,0)\) (set \(\alpha = 0\))

Fig. 53 The span of \((1,1)\) in \(\mathbb{R}^2\)#

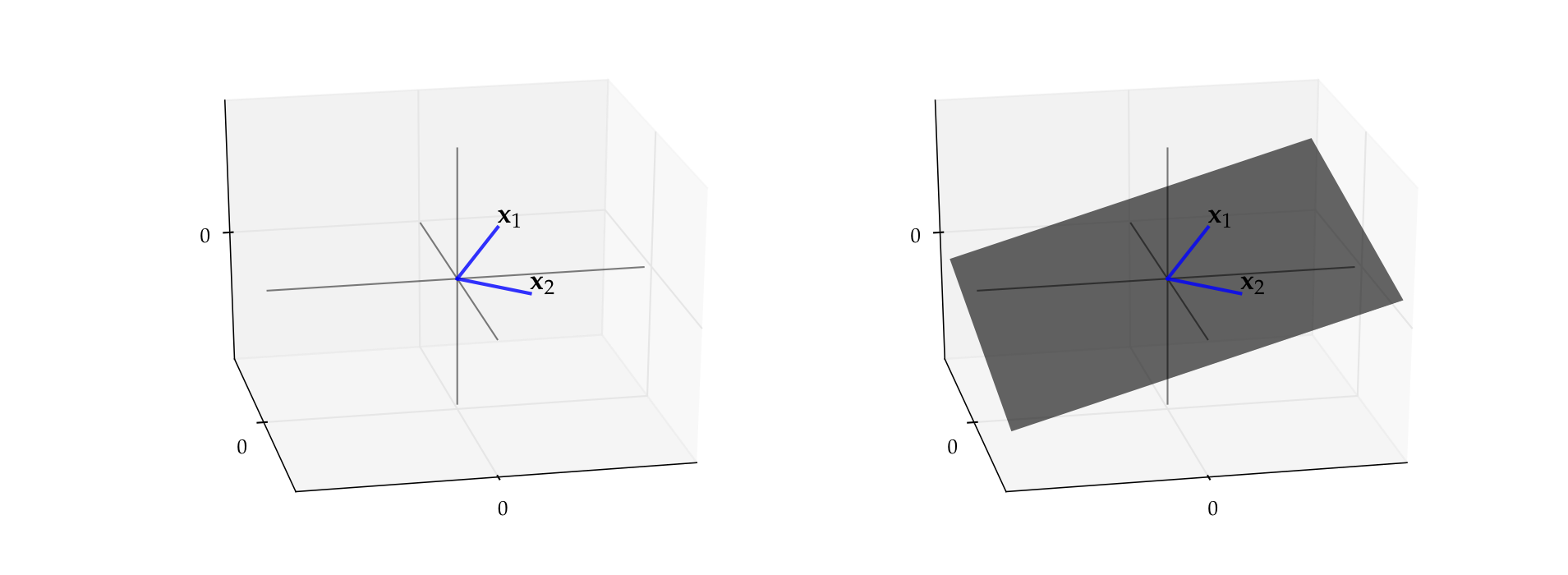

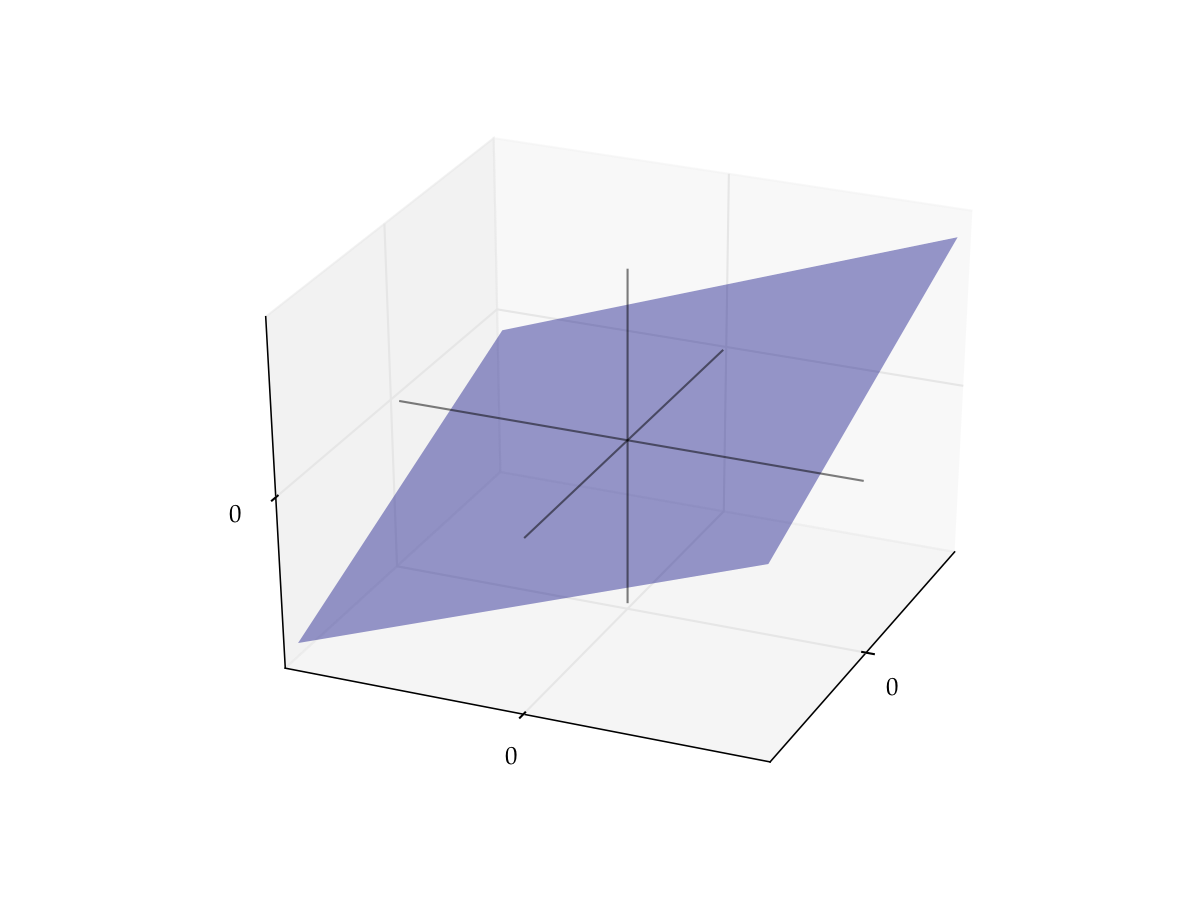

Example

Let \(x_1 = (3, 4, 2)\) and let \(x_2 = (3, -4, 0.4)\)

By definition, the span is all vectors of the form

It turns out to be a plane that passes through

the vector \(x_1\)

the vector \(x_2\)

the origin \(0\)

Fig. 54 Span of \(x_1, x_2\)#

Definition

Consider the vectors \(\{e_1, \ldots, e_N\} \subset \mathbb{R}^N\), where

That is, \(e_n\) has all zeros except for a \(1\) as the \(n\)-th element

Vectors \(e_1, \ldots, e_N\) are called the canonical basis vectors of \(\mathbb{R}^N\)

Fig. 55 Canonical basis vectors in \(\mathbb{R}^2\)#

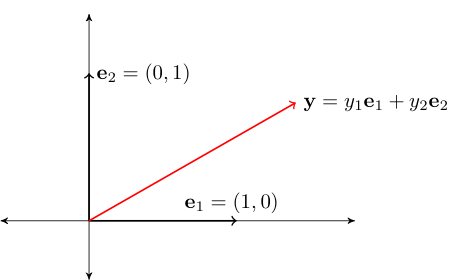

Fact

The span of \(\{e_1, \ldots, e_N\}\) is equal to all of \(\mathbb{R}^N\)

Proof

Proof for \(N=2\):

Pick any \(y \in \mathbb{R}^2\)

We have

Thus, \(y \in \mathrm{span} \{e_1, e_2\}\)

Since \(y\) arbitrary, we have shown that \(\mathrm{span} \{e_1, e_2\} = \mathbb{R}^2\)

Fig. 56 Canonical basis vectors in \(\mathbb{R}^2\)#

Linear subspace#

Definition

A nonempty \(S \subset \mathbb{R}^N\) called a linear subspace of \(\mathbb{R}^N\) if

In other words, \(S \subset \mathbb{R}^N\) is “closed” under vector addition and scalar multiplication

Note: Sometimes we just say subspace and drop “linear”

Example

\(\mathbb{R}^N\) itself is a linear subspace of \(\mathbb{R}^N\)

Fact

Fix \(a \in \mathbb{R}^N\) and let \(A = \{ x \in \mathbb{R}^N \colon a 'x = 0 \}\)

The set \(A\) is a linear subspace of \(\mathbb{R}^N\)

Proof

Let \(x, y \in A\) and let \(\alpha, \beta \in \mathbb{R}\)

We must show that \(z = \alpha x + \beta y \in A\)

Equivalently, that \(a^T z = 0\)

True because

Linear independence#

Definition

A nonempty collection of vectors \(X = \{x_1,\ldots, x_K\} \subset \mathbb{R}^N\) is called linearly independent if

linear independence of a set of vectors determines how large a space they span

loosely speaking, linearly independent sets span large spaces

Example

Let \(x = (1, 2)\) and \(y = (-5, 3)\)

The set \(X = \{x, y\}\) is linearly independent in \(\mathbb{R}^2\)

Indeed, suppose \(\alpha_1\) and \(\alpha_2\) are scalars with

Equivalently,

Then \(2(5\alpha_2) = 10 \alpha_2 = -3 \alpha_2\), implying \(\alpha_2 = 0\) and hence \(\alpha_1 = 0\)

Fact

The set of canonical basis vectors \(\{e_1, \ldots, e_N\}\) is linearly independent in \(\mathbb{R}^N\)

Proof

Let \(\alpha_1, \ldots, \alpha_N\) be coefficients such that \(\sum_{k=1}^N \alpha_k e_k = 0\)

Then

In particular, \(\alpha_k = \) for all \(k\)

Hence \(\{e_1, \ldots, e_N\}\) linearly independent

\(\blacksquare\)

Fact

Take \(X = \{x_1,\ldots, x_K\} \subset \mathbb{R}^N\). For \(K > 1\) all of following statements are equivalent

\(X\) is linearly independent

No \(x_i \in X\) can be written as linear combination of the others

\(X_0 \subset X \implies \mathrm{span}(X_0) \subset \mathrm{span}(X)\)

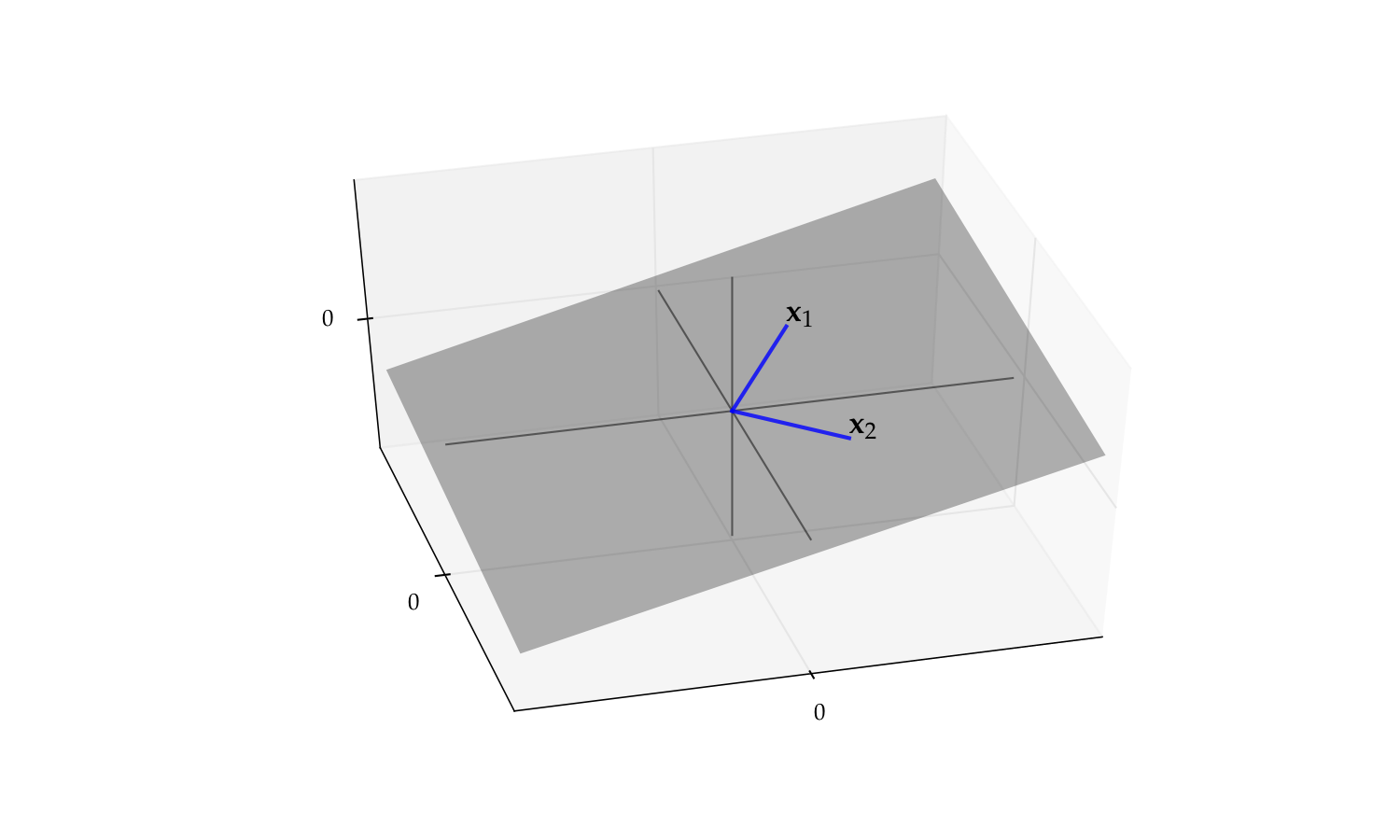

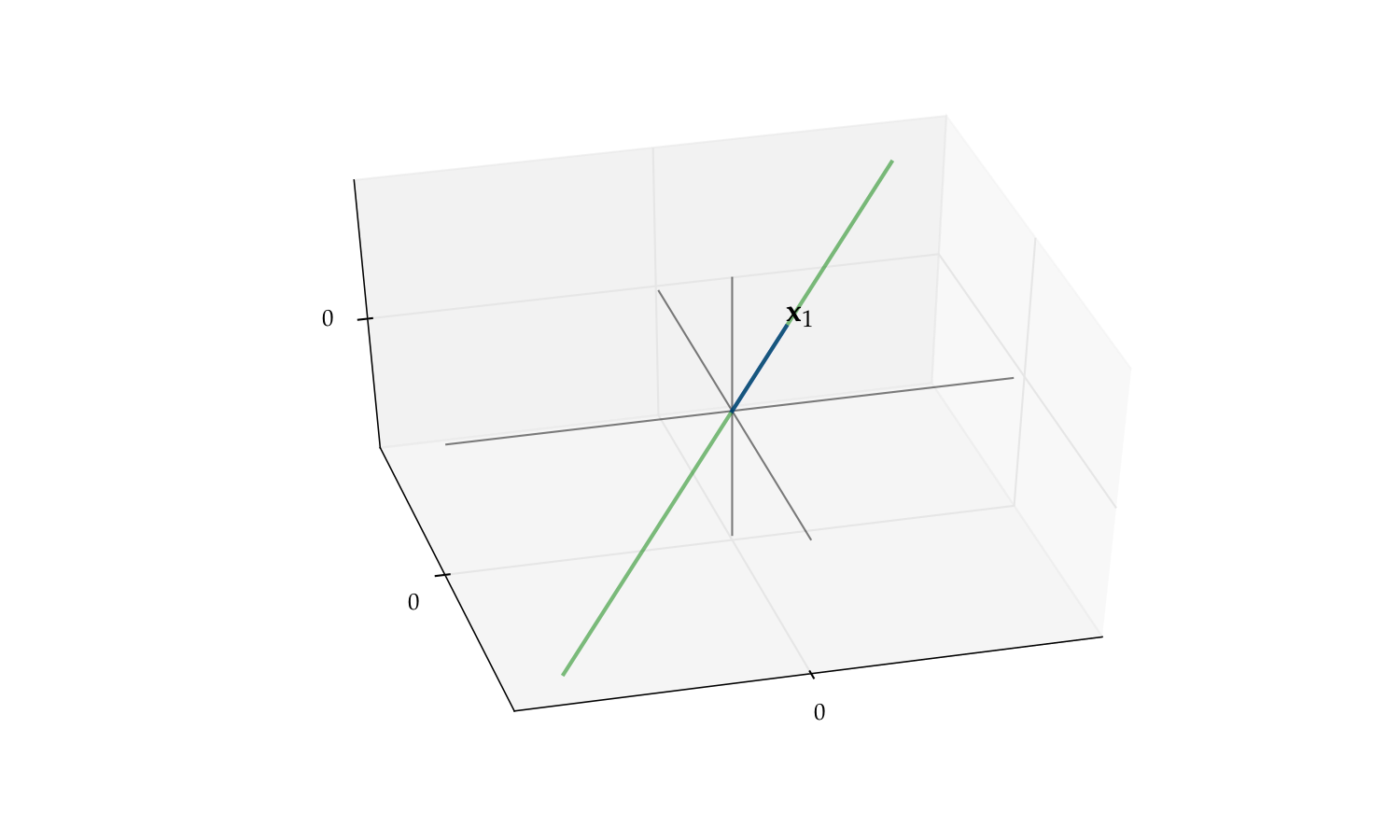

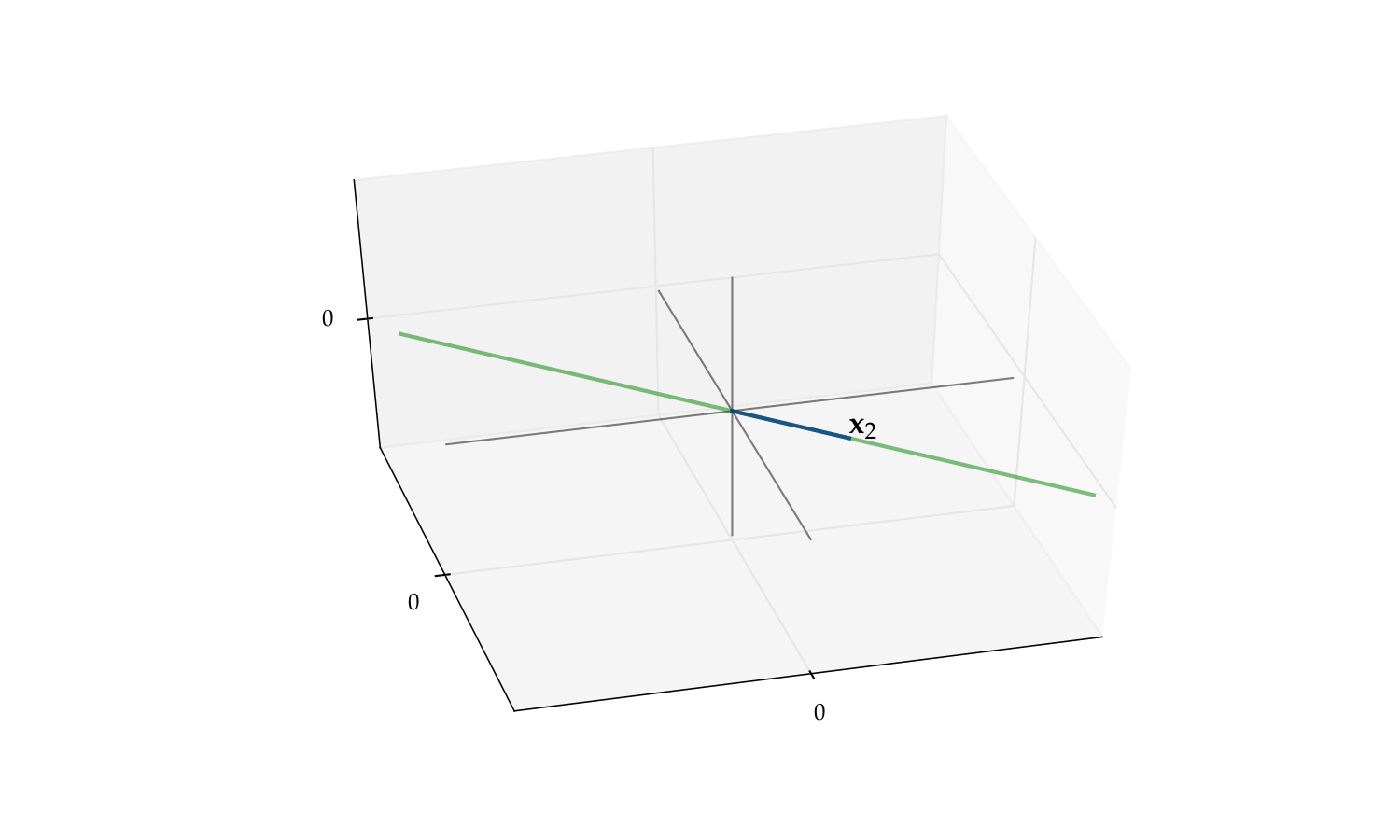

Example

As another visual example of linear independence, consider the pair

The span of this pair is a plane in \(\mathbb{R}^3\)

But if we drop either one the span reduces to a line

Fig. 57 The span of \(\{x_1, x_2\}\) is a plane#

Fig. 58 The span of \(\{x_1\}\) alone is a line#

Fig. 59 The span of \(\{x_2\}\) alone is a line#

Fact

If \(X\) is linearly independent, then \(X\) does not contain \(0\)

Proof

Exercise

Fact

If \(X\) is linearly independent, then every subset of \(X\) is linearly independent

Proof

Sketch of proof: Suppose for example that \(\{x_1,\ldots, x_{K-1}\} \subset X\) is linearly dependent

Then \(\exists \; \alpha_1, \ldots, \alpha_{K-1}\) not all zero with \(\sum_{k=1}^{K-1} \alpha_k x_k = 0\)

Setting \(\alpha_K =0\) we can write this as \(\sum_{k=1}^K \alpha_k x_k = 0\)

Not all scalars zero so contradicts linear independence of \(X\)

Fact

If \(X= \{x_1,\ldots, x_K\} \subset \mathbb{R}^N\) is linearly independent and \(z\) is an \(N\)-vector not in \(\mathrm{span}(X)\), then \(X \cup \{ z \}\) is linearly independent

Proof

Suppose to the contrary that \(X \cup \{ z \}\) is linearly dependent:

If \(\beta=0\), then we have \(\sum_{k=1}^K \alpha_k x_k = 0\) and \(\alpha_k \ne 0\) for some \(k\), a contradiction

If \(\beta \ne0\), then by we have

Hence \(z \in \mathrm{span}(X)\) — contradiction

Fact

If \(X = \{x_1,\ldots, x_K\} \subset \mathbb{R}^N\) is linearly independent and \(y \in \mathbb{R}^N\), then there is at most one set of scalars \(\alpha_1,\ldots,\alpha_K\) such that \(y = \sum_{k=1}^K \alpha_k x_k\)

Proof

Suppose there are two such sets of scalars

That is,

Here’s one of the most fundamental results in linear algebra

Exchange Lemma

Let \(S\) be a linear subspace of \(\mathbb{R}^N\), and be spanned by \(K\) vectors.

Then any linearly independent subset of \(S\) has at most \(K\)

vectors

Proof

Omitted

Example

If \(X = \{x_1, x_2, x_3\} \subset \mathbb{R}^2\), then \(X\) is linearly dependent

because \(\mathbb{R}^2\) is spanned by the two vectors \(e_1, e_2\)

Fig. 60 Must be linearly dependent#

Fact

Let \(X = \{ x_1, \ldots, x_N \}\) be any \(N\) vectors in \(\mathbb{R}^N\)

\(\mathrm{span}(X) = \mathbb{R}^N\) if and only if \(X\) is linearly independent

Example

The vectors \(x = (1, 2)\) and \(y = (-5, 3)\) span \(\mathbb{R}^2\)

Proof

Let prove that

\(X= \{ x_1, \ldots, x_N \}\) linearly independent \(\implies\) \(\mathrm{span}(X) = \mathbb{R}^N\)

Seeking a contradiction, suppose that

\(X \) is linearly independent

and yet \(\exists \, z \in \mathbb{R}^N\) with \(z \notin \mathrm{span}(X)\)

But then \(X \cup \{z\} \subset \mathbb{R}^N\) is linearly independent (why?)

This set has \(N+1\) elements

And yet \(\mathbb{R}^N\) is spanned by the \(N\) canonical basis vectors

Contradiction (of what?)

Next let’s show the converse

\(\mathrm{span}(X) = \mathbb{R}^N\) \(\implies\) \(X= \{ x_1, \ldots, x_N \}\) linearly independent

Seeking a contradiction, suppose that

\(\mathrm{span}(X) = \mathbb{R}^N\)

and yet \(X\) is linearly dependent

Since \(X\) not independent, \(\exists X_0 \subsetneq X\) with \(\mathrm{span}(X_0) = \mathrm{span}(X)\)

But by 1 this implies that \(\mathbb{R}^N\) is spanned by \(K < N\) vectors

But then the \(N\) canonical basis vectors must be linearly dependent

Contradiction

Bases and dimension#

Definition

Let \(S\) be a linear subspace of \(\mathbb{R}^N\)

A set of vectors \(B = \{b_1, \ldots, b_K\} \subset S\) is called a basis of \(S\) if

\(B\) is linearly independent

\(\mathrm{span}(B) = S\)

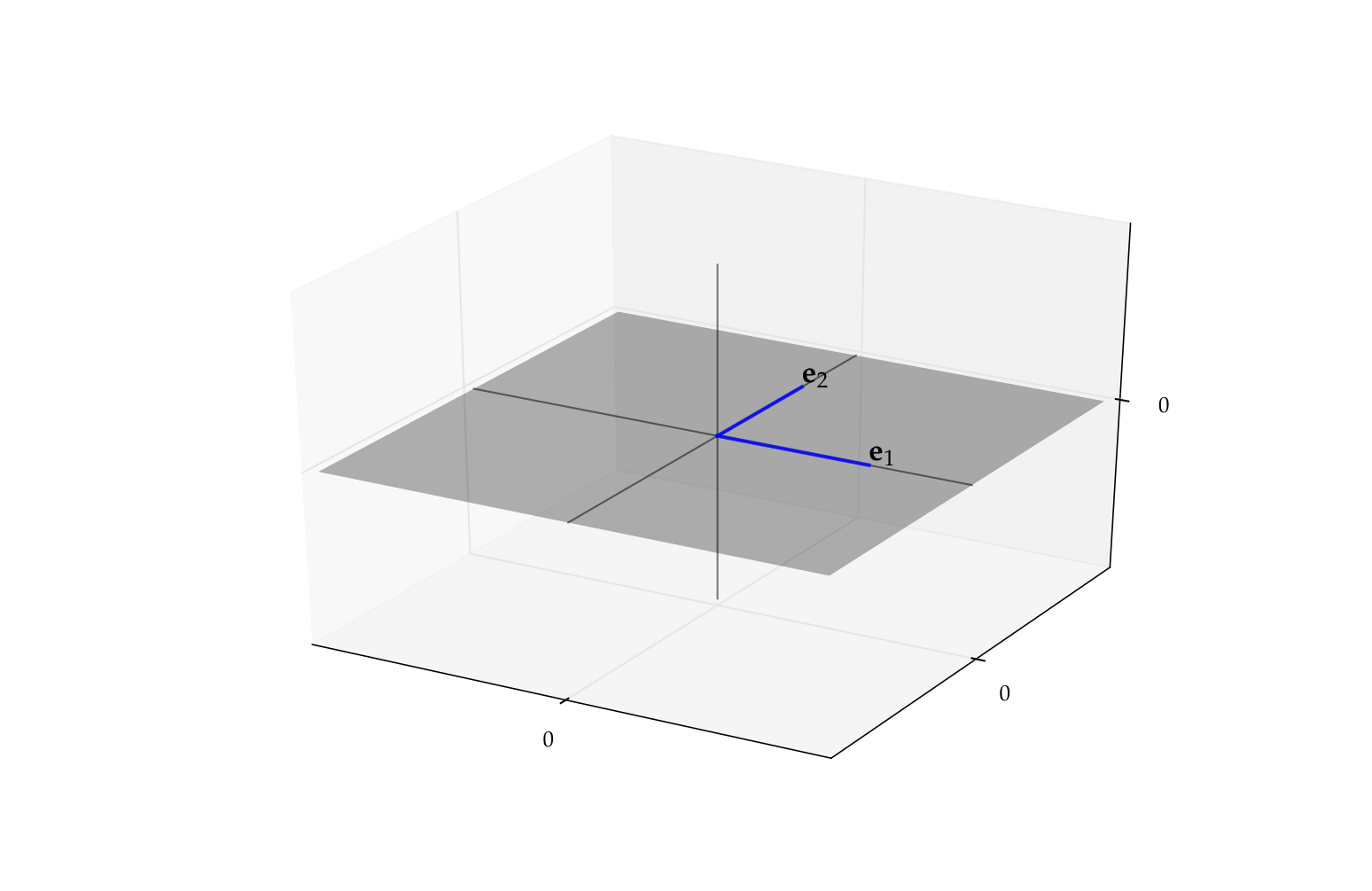

Example

Canonical basis vectors form a basis of \(\mathbb{R}^N\)

Example

Recall the plane

We showed before that \(\mathrm{span}\{e_1, e_2\} = P\) for

Moreover, \(\{e_1, e_2\}\) is linearly independent (why?)

Hence \(\{e_1, e_2\}\) is a basis for \(P\)

Fig. 61 The pair \(\{e_1, e_2\}\) form a basis for \(P\)#

What are the implications of \(B\) being a basis of \(S\)?

every element of \(S\) can be represented uniquely from the smaller set \(B\)

In more detail:

\(B\) spans \(S\) and, by linear independence, every element is needed to span \(S\) — a “minimal” spanning set

Since \(B\) spans \(S\), every \(y\) in \(S\) can be represented as a linear combination of the basis vectors

By independence, this representation is unique

Fact

If \(B \subset \mathbb{R}^N\) is linearly independent, then \(B\) is a basis of \(\mathrm{span}(B)\)

Proof

Follows from the definitions

Fact: Fundamental Properties of Bases

If \(S\) is a linear subspace of \(\mathbb{R}^N\) distinct from \(\{0\}\), then

\(S\) has at least one basis, and

every basis of \(S\) has the same number of elements

Proof

Proof of part 2: Let \(B_i\) be a basis of \(S\) with \(K_i\) elements, \(i=1, 2\)

By definition, \(B_2\) is a linearly independent subset of \(S\)

Moreover, \(S\) is spanned by the set \(B_1\), which has \(K_1\) elements

Hence \(K_2 \leq K_1\)

Reversing the roles of \(B_1\) and \(B_2\) gives \(K_1 \leq K_2\)

Definition

Let \(S\) be a linear subspace of \(\mathbb{R}^N\)

We now know that every basis of \(S\) has the same number of elements

This common number is called the dimension of \(S\)

Example

\(\mathbb{R}^N\) is \(N\) dimensional because the \(N\) canonical basis vectors form a basis

Example

\(P = \{ (x_1, x_2, 0) \in \mathbb{R}^3 \colon x_1, x_2 \in \mathbb{R \}}\) is two dimensional because the first two canonical basis vectors of \(\mathbb{R}^3\) form a basis

Linear Mappings#

Linear functions are in one-to-one correspondence with matrices

Nonlinear functions are closely connected to linear functions through Taylor approximation

Definition

A function \(T \colon \mathbb{R}^K \to \mathbb{R}^N\) is called linear if

Linear functions often written with upper case letters

Typically omit parenthesis around arguments when convenient

Example

\(T \colon \mathbb{R} \to \mathbb{R}\) defined by \(Tx = 2x\) is linear

Proof

Take any \(\alpha, \beta, x, y\) in \(\mathbb{R}\) and observe that

Example

The function \(f \colon \mathbb{R} \to \mathbb{R}\) defined by \(f(x) = x^2\) is nonlinear

Proof

Set \(\alpha = \beta = x = y = 1\)

Then

\(f(\alpha x + \beta y) = f(2) = 4\)

But \(\alpha f(x) + \beta f(y) = 1 + 1 = 2\)

Example

Given constants \(c_1\) and \(c_2\), the function \(T \colon \mathbb{R}^2 \to \mathbb{R}\) defined by

is linear

Proof

If we take any \(\alpha, \beta\) in \(\mathbb{R}\) and \(x, y\) in \(\mathbb{R}^2\), then

Fig. 62 The graph of \(T x = c_1 x_1 + c_2 x_2\) is a plane through the origin#

Note

Thinking of linear functions as those whose graph is a straight line is not correct!

Example

Function \(f \colon \mathbb{R} \to \mathbb{R}\) defined by \(f(x) = 1 + 2x\) is nonlinear

Proof

Take \(\alpha = \beta = x = y = 1\)

Then

\(f(\alpha x + \beta y) = f(2) = 5\)

But \(\alpha f(x) + \beta f(y) = 3 + 3 = 6\)

This kind of function is called an affine function

Fact

If \(T \colon \mathbb{R}^K \to \mathbb{R}^N\) is a linear mapping and \(x_1,\ldots, x_J\) are vectors in \(\mathbb{R}^K\), then for any linear combination we have

Proof

Proof for \(J=3\): Applying the def of linearity twice,

Fact

If \(T \colon \mathbb{R}^K \to \mathbb{R}^N\) is a linear mapping, then

Here \(e_k\) is the \(k\)-th canonical basis vector in \(\mathbb{R}^K\)

note that \(V = \{Te_1, \ldots, Te_K\}\) is the set of columns of the matrix representation of \(T\)

Proof

Any \(x \in \mathbb{R}^K\) can be expressed as \(\sum_{k=1}^K \alpha_k e_k\)

Hence \(\mathrm{rng}(T)\) is the set of all points of the form

as we vary \(\alpha_1, \ldots, \alpha_K\) over all combinations

This coincides with the definition of \(\mathrm{span}(V)\)

Example

Let \(T \colon \mathbb{R}^2 \to \mathbb{R}^2\) be defined by

Then

Exercise: Show that \(V = \{Te_1, Te_2\}\) is linearly independent

We conclude that the range of \(T\) is all of \(\mathbb{R}^2\) (why?)

Definition

The null space or kernel of linear mapping \(T \colon \mathbb{R}^K \to \mathbb{R}^N\) is

Linearity and Bijections#

Recall that an arbitrary function can be

one-to-one (injections)

onto (surjections)

both (bijections)

neither

For linear functions from \(\mathbb{R}^N\) to \(\mathbb{R}^N\), the first three are all equivalent!

In particular,

Fact

If \(T\) is a linear function from \(\mathbb{R}^N\) to \(\mathbb{R}^N\) then all of the following are equivalent:

\(T\) is a bijection

\(T\) is onto/surjective

\(T\) is one-to-one/injective

\(\mathrm{kernel}(T) = \{ 0 \}\)

The set of vectors \(V = \{Te_1, \ldots, Te_N\}\) is linearly independent

Definition

If any one of the above equivalent conditions is true, then \(T\) is called nonsingular

Proof

Proof that \(T\) onto \(\iff\) \(V = \{Te_1, \ldots, Te_N\}\) is linearly independent

Recall that for any linear mapping \(T\) we have \(\mathrm{rng}(T) = \mathrm{span}(V)\)

Using this fact and the definitions,

(We saw that \(N\) vectors span \(\mathbb{R}^N\) iff linearly indepenent)

Exercise: rest of proof

Fact

If \(T \colon \mathbb{R}^N \to \mathbb{R}^N\) is nonsingular then so is \(T^{-1}\).

Proof

Exercise: prove this statement

Mappings Across Different Dimensions#

Remember that the above results apply to mappings from \(\mathbb{R}^N\) to \(\mathbb{R}^N\)

Things change when we look at linear mappings across dimensions

The general rules for linear mappings are

Mappings from lower to higher dimensions cannot be onto

Mappings from higher to lower dimensions cannot be one-to-one

In either case they cannot be bijections

Fact

For a linear mapping \(T\) from \(\mathbb{R}^K \to \mathbb{R}^N\), the following statements are true:

If \(K < N\) then \(T\) is not onto

If \(K > N\) then \(T\) is not one-to-one

Proof

Proof of part 1: Let \(K < N\) and let \(T \colon \mathbb{R}^K \to \mathbb{R}^N\) be linear

Letting \(V = \{Te_1, \ldots, Te_K\}\), we have

Hence \(T\) is not onto

Proof of part 2: \(K > N\) \(\implies\) \(T\) is not one-to-one

Suppose to the contrary that \(T\) is one-to-one

Let \(\alpha_1, \ldots, \alpha_K\) be a collection of vectors such that

We have shown that \(\{Te_1, \ldots, Te_K\}\) is linearly independent

But then \(\mathbb{R}^N\) contains a linearly independent set with \(K > N\) vectors — contradiction

Example

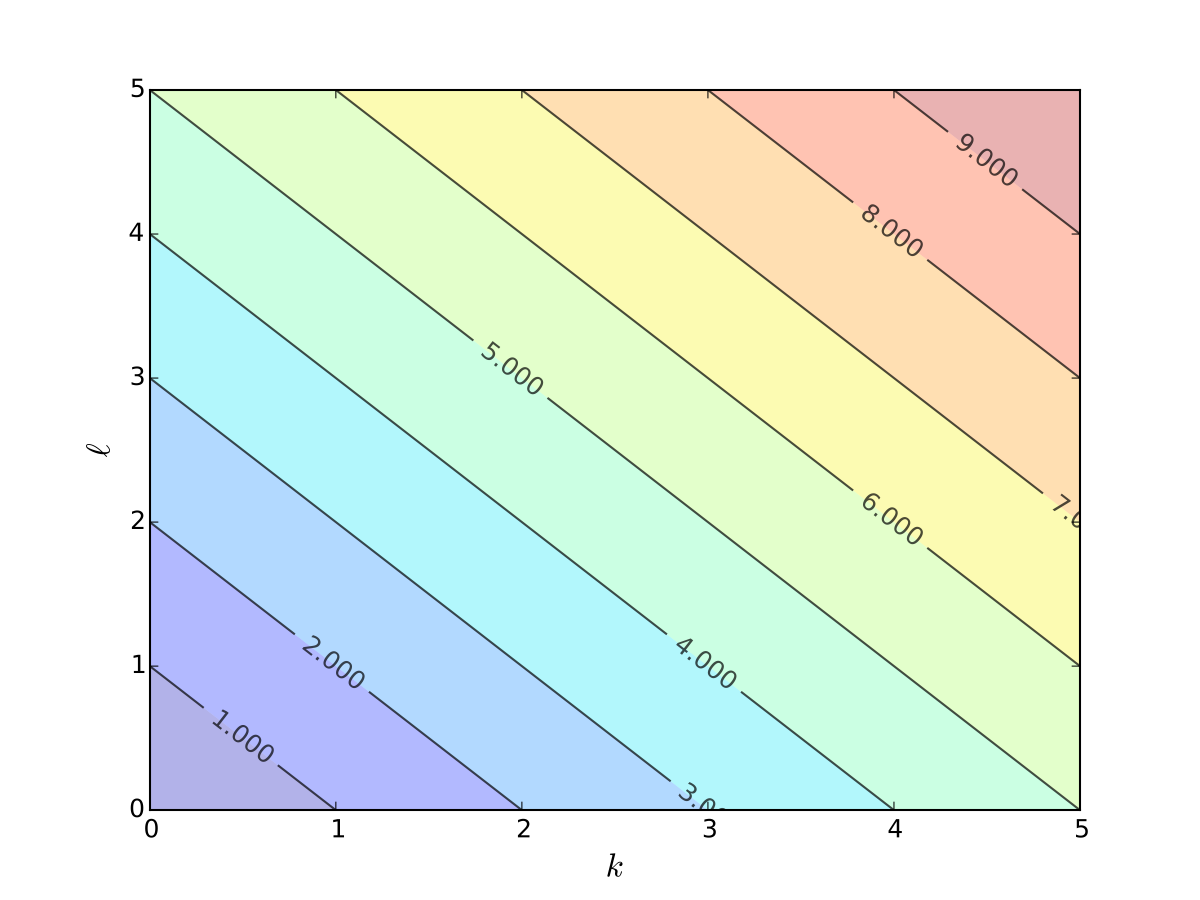

Cost function \(c(k, \ell) = rk + w\ell\) cannot be one-to-one

Matrices as Mappings#

Any \(N \times K\) matrix \(A\) can be thought of as a function \(x \mapsto A x\)

In \(A x\) the \(x\) is understood to be a column vector

It turns out that every such mapping is linear!

To see this fix \(N \times K\) matrix \(A\) and let \(T\) be defined by

Pick any \(x\), \(y\) in \(\mathbb{R}^K\), and any scalars \(\alpha\) and \(\beta\)

The rules of matrix arithmetic tell us that

So matrices make linear functions

How about examples of linear functions that don’t involve matrices?

There are none!

Fact

If \(T \colon \mathbb{R}^K \to \mathbb{R}^N\) then

Proof

Just above we showed the \(\Longleftarrow\) part

Let’s show the \(\implies\) part

Let \(T \colon \mathbb{R}^K \to \mathbb{R}^N\) be linear

We aim to construct an \(N \times K\) matrix \(A\) such that

As usual, let \(e_k\) be the \(k\)-th canonical basis vector in \(\mathbb{R}^K\)

Define a matrix \(A\) by \(\mathrm{col}_k(A) = Te_k\)

Pick any \(x = (x_1, \ldots, x_K) \in \mathbb{R}^K\)

By linearity we have

Matrix Product as Composition#

Fact

Let

\(A\) be \(N \times K\) and \(B\) be \(K \times M\)

\(T \colon \mathbb{R}^K \to \mathbb{R}^N\) be the linear mapping \(Tx = Ax\)

\(U \colon \mathbb{R}^M \to \mathbb{R}^K\) be the linear mapping \(Ux = Bx\)

The matrix product \(A B\) corresponds exactly to the composition of \(T\) and \(U\)

Proof

This helps us understand a few things

For example, let

\(A\) be \(N \times K\) and \(B\) be \(J \times M\)

\(T \colon \mathbb{R}^K \to \mathbb{R}^N\) be the linear mapping \(Tx = Ax\)

\(U \colon \mathbb{R}^M \to \mathbb{R}^J\) be the linear mapping \(Ux = Bx\)

Then \(A B\) is only defined when \(K = J\)

This is because \(A B\) corresponds to \(T \circ U\)

But for \(T \circ U\) to be well defined we need \(K = J\)

Then \(U\) mappings \(\mathbb{R}^M\) to \(\mathbb{R}^K\) and \(T\) mappings \(\mathbb{R}^K\) to \(\mathbb{R}^N\)

Column Space#

Definition

Let \(A\) be an \(N \times K\) matrix.

The column space of \(A\) is defined as the span of its columns

Equivalently,

This is exactly the range of the associated linear mapping

\(T \colon \mathbb{R}^K \to \mathbb{R}^N\) defined by \(T x = A x\)

Example

If

then the span is all linear combinations

These columns are linearly independent (shown earlier)

Hence the column space is all of \(\mathbb{R}^2\) (why?)

Exercise: Show that the column space of any \(N \times K\) matrix is a linear subspace of \(\mathbb{R}^N\)

Rank#

Equivalent questions

How large is the range of the linear mapping \(T x = A x\)?

How large is the column space of \(A\)?

The obvious measure of size for a linear subspace is its dimension

Definition

The dimension of \(\mathrm{span}(A)\) is known as the rank of \(A\)

Because \(\mathrm{span}(A)\) is the span of \(K\) vectors, we have

Definition

\(A\) is said to have full column rank if

Fact

For any matrix \(A\), the following statements are equivalent:

\(A\) is of full column rank

The columns of \(A\) are linearly independent

If \(A x = 0\), then \(x = 0\)

Exercise: Check this, recalling that

import numpy as np

A = [[2.0, 1.0],

[6.5, 3.0]]

print(f'Rank = {np.linalg.matrix_rank(A)}')

A = [[2.0, 1.0],

[6.0, 3.0]]

print(f'Rank = {np.linalg.matrix_rank(A)}')

Rank = 2

Rank = 1

Systems of Linear Equations#

Let’s look at solving linear equations such as \(A x = b\) where \(A\) is a square matrix

Take \(N \times N\) matrix \(A\) and \(N \times 1\) vector \(b\) as given

Search for an \(N \times 1\) solution \(x\)

But does such a solution exist? If so is it unique?

The best way to think about this is to consider the corresponding linear mapping

Equivalent:

\(A x = b\) has a unique solution \(x\) for any given \(b\)

\(T x = b\) has a unique solution \(x\) for any given \(b\)

\(T\) is a bijection

We already have conditions for linear mappings to be bijections

Just need to translate these into the matrix setting

Recall that \(T\) called nonsingular if \(T\) is a linear bijection

Definition

We say that \(A\) is nonsingular if \(T: x \to Ax\) is nonsingular

Equivalent:

\(x \mapsto A x\) is a bijection from \(\mathbb{R}^N\) to \(\mathbb{R}^N\)

We now list equivalent conditions for nonsingularity

Fact

Let \(A\) be an \(N \times N\) matrix

All of the following conditions are equivalent

\(A\) is nonsingular

The columns of \(A\) are linearly independent

\(\mathrm{rank}(A) = N\)

\(\mathrm{span}(A) = \mathbb{R}^N\)

If \(A x = A y\), then \(x = y\)

If \(A x = 0\), then \(x = 0\)

For each \(b \in \mathbb{R}^N\), the equation \(A x = b\) has a solution

For each \(b \in \mathbb{R}^N\), the equation \(A x = b\) has a unique solution

All equivalent ways of saying that \(Tx = A x\) is a bijection!

Example

For condition 5 the equivalence is:

\(A x = A y\), then \(x = y\)

\(\iff\)

\(T x = T y\), then \(x = y\)

\(\iff\)

\(T\) is one-to-one

\(\iff\)

Since \(T\) is a linear mapping from \(\mathbb{R}^N\) to \(\mathbb{R}^N\),

\(T\) is a bijection

Example

For condition 6 the equivalence is:

if \(A x = 0\), then \(x = 0\)

\(\iff\)

\(\{x: Ax = 0\} = \{0\}\)

\(\iff\)

\(\{x: Tx = 0\} = \{0\}\)

\(\iff\)

\(\ker{T}=\{0\}\)

\(\iff\)

Since \(T\) is a linear mapping from \(\mathbb{R}^N\) to \(\mathbb{R}^N\),

\(T\) is a bijection

Example

For condition 7 the equivalence is:

for each \(b\in\mathbb{R}^N\), the equation \(Ax = b\) has a solution

\(\iff\)

every \(b\in\mathbb{R}^N\) has an \(x\) such that \(Ax = b\)

\(\iff\)

every \(b\in\mathbb{R}^N\) has an \(x\) such that \(Tx = b\)

\(\iff\)

\(T is onto/surjection\)

\(\iff\)

Since \(T\) is a linear mapping from \(\mathbb{R}^N\) to \(\mathbb{R}^N\),

\(T\) is a bijection

Example

Now consider condition 2: \

The columns of \(A\) are linearly independent.

Let \(e_j\) be the \(j\)-th canonical basis vector in \(\mathbb{R}^N\).

Observe that \(Ae_j = \mathrm{col}_j(A)\) \(\implies\) \(Te_j = \mathrm{col}_j(A)\) \(\implies\) \(V = \{T e_1, \ldots, Te_N\} =\) columns of \(A\), and \(V\) is linearly independent if and only if \(T\) is a bijection

Example

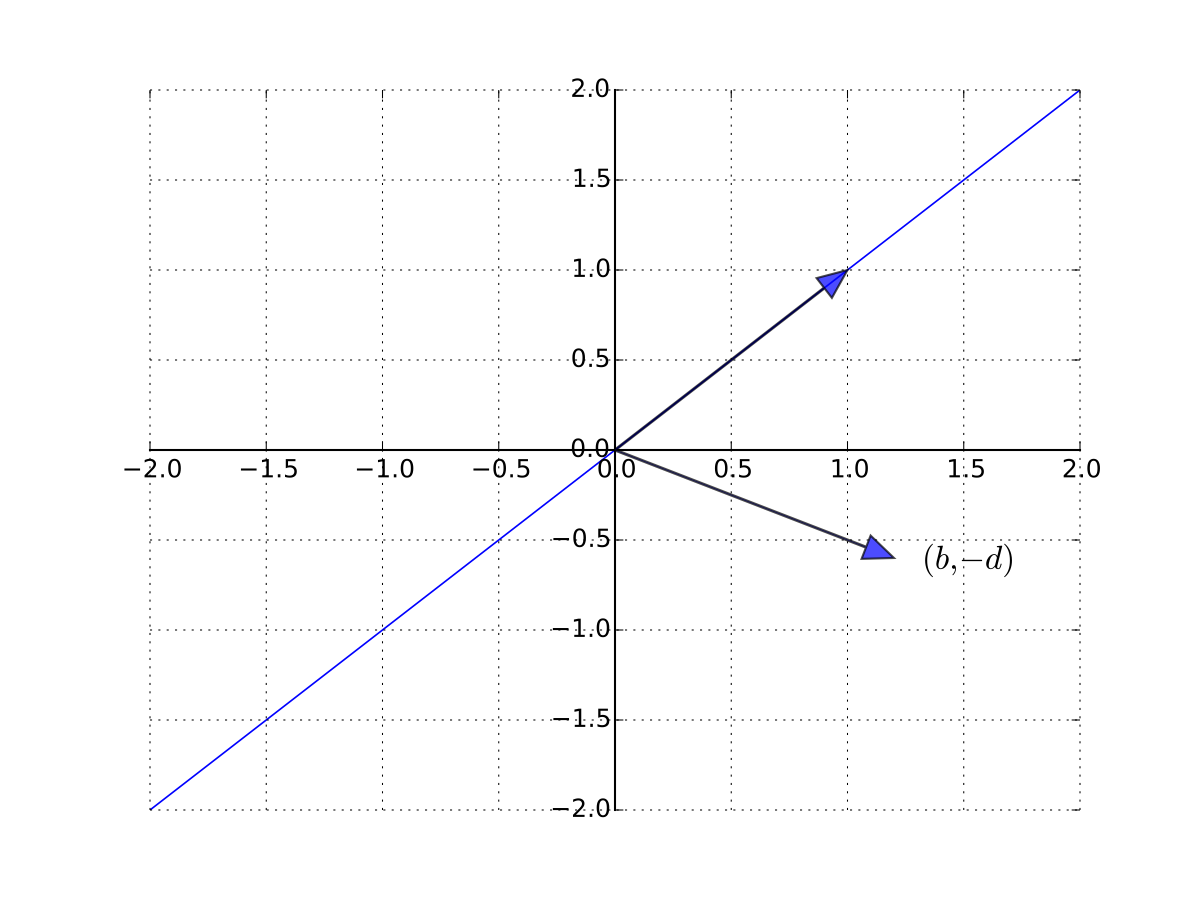

Consider a one good linear market system

Treating \(q\) and \(p\) as the unknowns, let’s write in matrix form as

A unique solution exists whenever the columns are linearly independent

so \((b, -d)\) is not a scalar multiple of \(1\) \(\iff\) \(b \ne -d\)

Fig. 63 \((b, -d)\) is not a scalar multiple of \(1\)#

Example

Recall in the introduction we try to solve the system \(A x = b\) of this form

The problem is that \(A\) is singular (not nonsingular)

In particular, \(\mathrm{col}_3(A) = 2 \mathrm{col}_2(A)\)

Definition

Given square matrix \(A\), suppose \(\exists\) square matrix \(B\) such that

Then

\(B\) is called the inverse of \(A\), and written \(A^{-1}\)

\(A\) is called invertible

Fact

A square matrix \(A\) is nonsingular if and only if it is invertible

\(A^{-1}\) is just the matrix corresponding to the linear mapping \(T^{-1}\)

Fact

Given nonsingular \(N \times N\) matrix \(A\) and \(b \in \mathbb{R}^N\), the unique solution to \(A x = b\) is given by

Proof

Since \(A\) is nonsingular we already know any solution is unique

\(T\) is a bijection, and hence one-to-one

if \(A x = A y = b\) then \(x = y\)

To show that \(x_b\) is indeed a solution we need to show that \(A x_b = b\)

To see this, observe that

Fact

In the \(2 \times 2\) case, the inverse has the form

Example

Fact

If \(A\) is nonsingular and \(\alpha \ne 0\), then

\(A^{-1}\) is nonsingular and \((A^{-1})^{-1} = A\)

\(\alpha A\) is nonsingular and \((\alpha A)^{-1} = \alpha^{-1} A^{-1}\)

Proof

Proof of part 2:

It suffices to show that \(\alpha^{-1} A^{-1}\) is the right inverse of \(\alpha A\)

This is true because

Fact

If \(A\) and \(B\) are \(N \times N\) and nonsingular then

\(A B\) is also nonsingular

\((A B)^{-1} = B^{-1} A^{-1}\)

Proof

Proof I: Let \(T\) and \(U\) be the linear mappings corresponding to \(A\) and \(B\)

Recall that

\(T \circ U\) is the linear mapping corresponding to \(A B\)

Compositions of linear mappings are linear

Compositions of bijections are bijections

Hence \(T \circ U\) is a linear bijection with \((T \circ U)^{-1} = U^{-1} \circ T^{-1}\)

That is, \(AB\) is nonsingular with inverse \(B^{-1} A^{-1}\)

Proof II:

A different proof that \(A B\) is nonsingular with inverse \(B^{-1} A^{-1}\)

Suffices to show that \(B^{-1} A^{-1}\) is the right inverse of \(A B\)

To see this, observe that

Hence \(B^{-1} A^{-1}\) is a right inverse as claimed

Singular case#

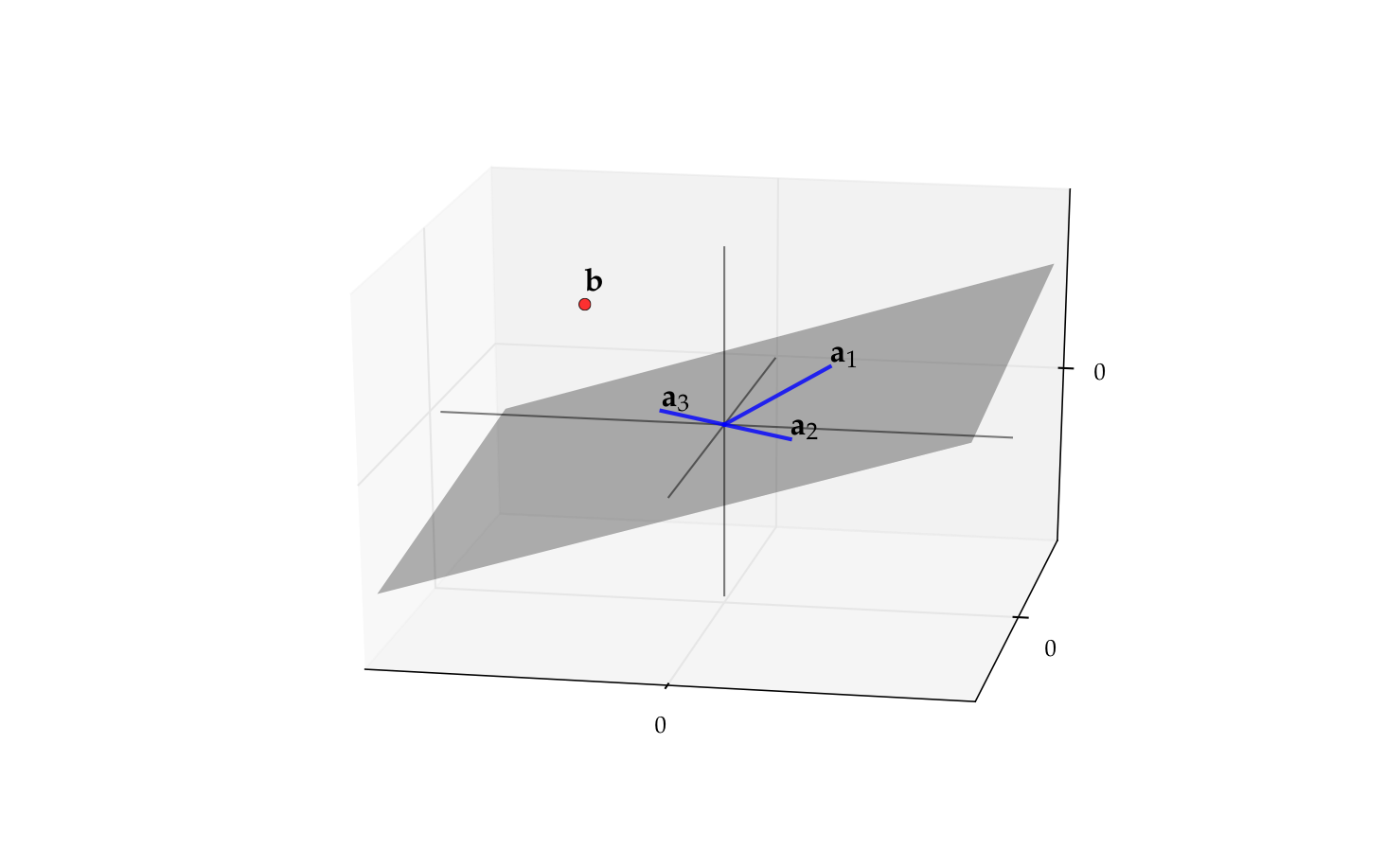

Example

The matrix \(A\) with columns

is singular (\(a_3 = - a_2\))

Its column space \(\mathrm{span}(A)\) is just a plane in \(\mathbb{R}^2\)

Recall \(b \in \mathrm{span}(A)\)

\(\iff\) \(\exists \, x_1, \ldots, x_N\) such that \(\sum_{k=1}^N x_k \mathrm{col}_k(A) = b\)

\(\iff\) \(\exists \, x\) such that \(A x = b\)

Thus if \(b\) is not in this plane then \(A x = b\) has no solution

Fig. 64 The vector \(b\) is not in \(\mathrm{span}(A)\)#

Fact

If \(A\) is a singular matrix and \(A x = b\) has a solution then it has an infinity (in fact a continuum) of solutions

Proof

Let \(A\) be singular and let \(x\) be a solution

Since \(A\) is singular there exists a nonzero \(y\) with \(A y = 0\)

But then \(\alpha y + x\) is also a solution for any \(\alpha \in \mathbb{R}\) because

References and reading#

References

[Simon and Blume, 1994]: 6.1, 6.2, 10.1, 10.2, 10.3, 10.4, 10.5, 10.6, 11, 16, 23.7, 23.8

[Sundaram, 1996]: Appendix C.1, C.2

Further reading and self-learning

Excellent visualizations of concepts covered in this lecture, strongly recommended for further study 3Blue1Brown: Essence of linear algebra